Introspection – September 2019 Parent Circle Article!

One of the most effective tools I have come across is Introspection. Through this process, we can correct ourselves, reflect upon what next?, what else?, what more?

In September 2019, we had an opportunity to write a half-page article in Parent Circle Magazine and here the contents:

Human Psychology – Buy Low, Sell High : Wonder how to make sure your returns are high while investing?

Our human tendency is to buy low and sell high, so that we make a profit. And when it comes to return on investments, we want maximum returns. We want liquidity as well. Unfortunately, this doesn’t always happen – be it in stock market or a fixed deposit scheme. Here is a scenario: You invest few lakhs in a two-year fixed deposit at 7.5% and within months, the interest rate goes up, and the same fixed deposit yields 7.75% or 8%. That can be disappointing. Same happens with equities. We buy a company stock at ‘x’ price and it goes down. We sell a stock at ‘y’ price and it goes up. How to then decide when to enter or when to exit? The easy way is to trust the professionals.

There are mutual funds that are run by professional managers, and

- They buy when the markets are at fair value (or) cheaper.

- They sell when the market valuations are high, and book profits.

- They invest across both equity and debt.

- They re-balance the portfolio at regular intervals, sometimes even daily.

These kinds of funds are called Balanced Advantage Funds. Fund houses like HDFC and ICICI have specific funds with this specific objective of “buying low and selling high”. Always consult a Certified Financial Planner before investing.

மனித உளவியல்: குறையும்போது வாங்கு; உயரும்போது விற்றுவிடு! .. முனைவர் ஏ.வி.செந்தில்.

உங்கள் முதலீடுகள் அதிக லாபத்தைக் கொடுப்பதை எப்படி உறுதி செய்யலாம்?

நமது மனித மனோபாவம் எப்படிப்பட்டது? குறைந்த விலைக்கு வாங்கி, அதிக விலைக்கு விற்பது லாபம் என்பதுதானே! முதலீடு என்கிற விஷயத்திலும் நீங்கள் அதிக லாபத்தைத்தானே எதிர்பார்ப்பீர்கள்? அதேநேரத்தில் முதலீடு, நினைத்த நேரத்தில் எடுத்துக்கொள்கிற மாதிரியும் இருக்க வேண்டும் இல்லையா! துரதிருஷ்டவசமான, இது பெரும்பாலும் பங்குச்சந்தை அல்லது ஃபிக்ஸட் டெபாஸிட் விஷயத்தில் நடப்பதில்லை.

ஒரு எடுத்துக்காட்டு: சில லட்சம் ரூபாயை நீங்கள் 2 ஆண்டுகளுக்கு (7.5% வட்டியில்) ஃபிக்ஸட் டெபாஸிட்டின் முதலீடு செய்கிறீர்கள். வட்டி வீதம் ஏறும்போது 7.57% (அ) 8% லாபம் கிடைக்கும். இது ஏமாற்றாத்தைத் தரலாம். இதுவேதான் பங்குச்சந்தையிலும் நடக்கும். ஒரு நிறுவனத்தின் பங்கை X என்ற விலையில் வாங்குகிறீர்கள். பங்கு மதிப்பு சரிகிறது. உடனே Y என்ற விலைக்கு அதனை விற்கிறீர்கள். உடனே விலை ஏறுகிறது. எப்போது விற்பது, எப்போது வாங்குவது என்ற குழப்பம் ஏற்படுகிறதா? கவலை வேண்டாம். வழிகாட்ட வல்லுநர்கள் இருக்கின்றனர்.

திறமையான நிர்வாகிகளைக்கொண்டு மியூச்சுவல் ஃபண்ட் திட்டங்கள் செயல்படுகின்றன.

அ)அவர்கள், எப்போது பங்குச்சந்தை சரிகிறதோ, அப்போது மலிவு விலைக்கு பங்குகளை வாங்குவர்.

ஆ)பங்கின் மதிப்பு உயரும்போது நல்ல லாபத்துக்கு விற்பர்.

இ)பங்குச்சந்தை, கடன் பத்திரங்கள் -ஆகிய இரண்டிலும் முதலீடு செய்வர்.

ஈ)தேவையானபோது (தினமும்கூட) முதலீட்டுத்திட்டத்தை அவர்கள் மாற்றியமைப்பர்.

இதுபோன்ற திட்டங்களை பேலன்ஸ்டு அட்வாண்டேஜ் ஃபண்ட் என்கிறோம். ஹெச்.டி.எஃப்.சி, ஐ.சி.ஐ.சி.ஐ போன்ற சில நிறுவனங்கள் ‘குறைந்தவிலைக்கு வாங்கி, அதிக லாபத்துக்கு விற்கும்’ திட்டங்களை வைத்திருக்கின்றன.

முதலீடு செய்வதற்குமுன் சான்றுபெற்ற நிதி ஆலோசகரை ஆலோசிக்கவும்.

Here is the reflection through the Introspection process:

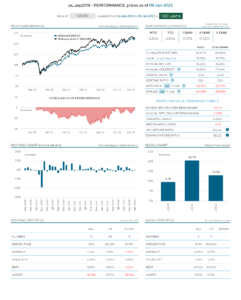

Assuming you had invested Rs. 50,000 each on Sep 15th 2019 in the above two funds (HDFC BAF – 50K and ICICI BAF – 50K), then this portfolio, would have given 60% absolute returns over 3 years and 3 months and the key data is summarized here.

Also when the markets are going up this portfolio captured 84% of the gains whereas when the markets are down, this portfolio fell only 80% (lower downside capture ratio) – So better returns at a lower risk!!!

With lower standard deviation (annual volatility of 14.6%) as compared to benchmark of 17.4% the portfolio delivered annualized returns of 15.3%, much higher the fixed deposits, tax free bonds, post office schemes and closer to equity benchmark returns, in spite of covid / pandemic in 2020 etc.

While we will not be able to predict the future and sometimes our investments may go down by 25% like in April 2020, patience, perseverance, advisor handholding play a vital role in achieving our financial goals.

If you would like us to review your portfolio, make changes to them, then do please reach out to us at cgo@avsenthil.com – You can do a google search on #avsenthil as well.

Happy investing 2023 and beyond!!

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully. The NAVs of the schemes may go up or down depending upon the factors and forces affecting the securities market including the fluctuations in the interest rates. The past performance of the mutual funds is not necessarily indicative of future performance of the schemes. The Mutual Fund is not guaranteeing or assuring any dividend under any of the schemes and the same is subject to the availability and adequacy of distributable surplus. Investors are requested to review the prospectus carefully and obtain expert professional advice with regard to specific legal, tax and financial implications of the investment/participation in the scheme.